Our investment and economic outlook, July 2024

.

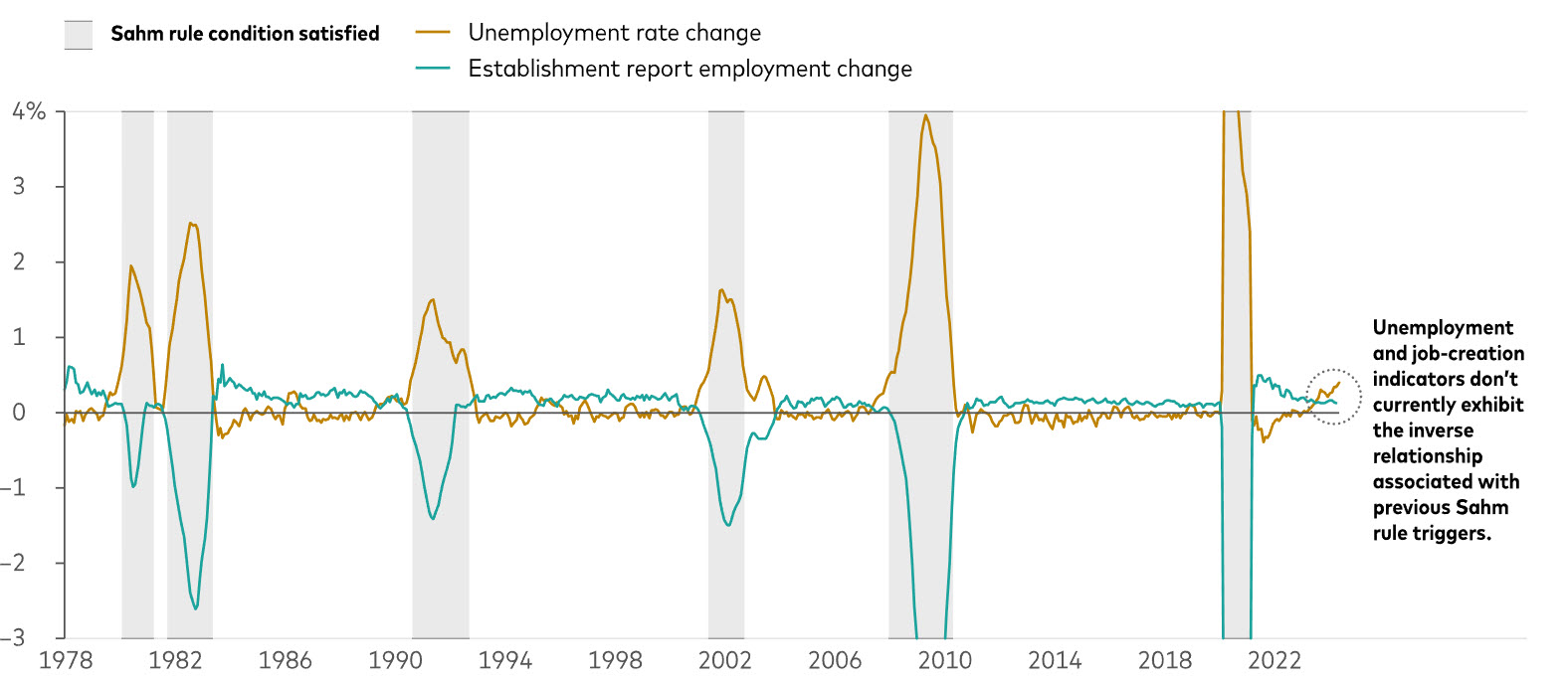

A labour market indicator that has reliably signaled the start of recession could appear in coming months. The Sahm rule (named after the former Federal Reserve economist who identified it) is triggered when the unemployment rate spikes, with its three-month moving average jumping half a percentage point above its 12-month trough. A 4.2% unemployment rate in the July jobs report, scheduled to be released 2 August, would do the trick. Would that mean a U.S. recession had started? Very doubtful, said Adam Schickling, a senior economist who studies the labour market.

An unfamiliar Sahm rule scenario

Notes: Unemployment rate change is measured as the three-month moving average unemployment rate minus the unemployment rate’s 12-month trough, as reflected in the monthly household survey conducted by the Bureau of Labour Statistics (BLS). Establishment report employment change is measured as the three-month moving average nonfarm employment level minus the nonfarm employment level 12-month maximum, as reflected in the monthly BLS establishment survey. Starting points for periods when the Sahm rule has been satisfied largely correspond to historical U.S. recessions. Historically, both the household and establishment surveys indicate labour market weakness during periods when Sahm rule conditions are met, with the unemployment rate rising and the number of jobs contracting, which isn’t the case currently.

Sources: Vanguard calculations using data as of 5 July, 2024, from the U.S. Bureau of Labor Statistics.

At issue, Schickling said, are the mixed signals being sent by the two surveys that make up the jobs report. “A significant and persistent deviation between the household and establishment surveys has created a unique paradox of the unemployment rate rising 60 basis points since July 2023 even as job creation in the establishment survey has more than offset an increase in the labour force.”

Declining response rates since the COVID-19 pandemic have affected all labour market surveys, Schickling said, but the effect on the household survey of workers and job candidates has been especially pronounced given that the survey was relatively small to begin with. Additionally, Vanguard believes that the separate establishment survey of workplaces is quicker than the household survey to reflect immigration dynamics that have fueled recent job growth. Because the Sahm rule uses unemployment rate metrics, it is based on the household survey, which we see as less reliable than it traditionally has been.

While its momentum has slowed, the labour market remains strong, and any imminent recession signal is likely to be a false one.

Outlook for financial markets

Our 10-year annualised nominal return and volatility forecasts are shown below. They are based on the 31 May, 2024, running of the Vanguard Capital Markets Model® (VCMM). Equity returns reflect a range of 2 percentage points around the 50th percentile of the distribution of probable outcomes. Fixed income returns reflect a 1-point range around the 50th percentile. More extreme returns are possible.

Australian dollar investors

- Australian equities: 4.7%–6.7% (21.9% median volatility)

- Global equities ex-Australia (unhedged): 4.4%–6.4% (19.2%)

- Australian aggregate bonds: 4.1%–5.1% (5.5%)

- Global bonds ex-Australia (hedged): 4.4%–5.4% (4.9%)

Notes: These probabilistic return assumptions depend on current market conditions and, as such, may change over time.

Source: Vanguard Investment Strategy Group.

IMPORTANT: The projections or other information generated by the Vanguard Capital Markets Model regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. Distribution of return outcomes from the VCMM are derived from 10,000 simulations for each modelled asset class. Simulations are as of 31 May, 2024. Results from the model may vary with each use and over time.

Region-by-region outlook

The views below are those of the global economics and markets team of Vanguard Investment Strategy Group as of 17 July, 2024.

Australia

Lacklustre GDP growth in the first quarter suggests that restrictive monetary policy has curbed demand. Yet low productivity growth has kept unit labour costs growing at a rate well above that which is consistent with the 2%–3% inflation target set by the Reserve Bank of Australia (RBA). As such, the RBA may be one of the last developed markets central banks to ease monetary policy.

We believe that if inflation returns to more sustainable levels, Australia’s slow growth will open the door to monetary policy easing. Despite sticky inflation, we don’t foresee a rate hike by the RBA, whose dual mandate is to promote price stability and economic growth.

- GDP rose by just 0.1% in the first quarter on a seasonally adjusted basis and by 1.1% year over year. A softening in demand is especially notable considering Australia’s population growth, which has been supported by immigration. Growth in Australia’s immigrant population was more than five times natural population growth in 2023. On a per-capita basis, first-quarter GDP was down by 0.4% quarter over quarter and by 1.3% year over year.

- Inflation has remained elevated. Year-over-year headline inflation continued an upward trajectory in May, rising to 4.0% from 3.6% in April. Trimmed mean inflation, a measure of core inflation that strips out items at the extremes, also accelerated, to 4.4% year over year in May from 4.1% in April, a fourth straight month of year-over-year increases.

- We expect the unemployment rate to rise to around 4.6% by the end of 2024 as financial conditions tighten in an environment of elevated interest rates. It was 4.0% in May.

United States

The productivity and labour supply gains that drove U.S. economic growth in 2023 lately show signs of subsiding, joining retail sales, capital expenditure, and other data that previously suggested a slowdown.

- The Federal Reserve Bank of Atlanta’s GDP Now tracker suggests the U.S. economy grew by 2.5% in the second quarter, but proprietary Vanguard models foresee lower growth. We continue to anticipate full-year GDP growth around 2%.

- A second straight benign Consumer Price Index reading cheered markets, which now anticipate a quarter-point Fed interest rate cut in September. Vanguard’s base case is that the Fed will still find it is unable to cut interest rates in 2024 if shelter inflation remains prohibitively high, as Josh Hirt, a Vanguard senior economist, recently discussed. However, continued favorable inflation readings will likely move a rate cut forward, with September as the most likely timing.

- We expect the Fed’s preferred inflation measure, the core Personal Consumption Expenditures price index, to rise to 2.9% by year-end because of challenging comparisons with year-earlier data. It was 2.6% on a year-over-year basis in May.

- Vanguard believes that the Fed will need to see continued supportive inflation data or a sharp slowdown in the labour market before it cuts interest rates. Should the Fed decide to cut interest rates in 2024, we don’t foresee more than a single quarter-point cut. It faces a tricky balance between cutting rates too soon and risking resurgent inflation, and cutting too late to the economy’s detriment.

Canada

Given progress in the inflation fight and below-trend economic growth, the Bank of Canada (BOC) on 5 June became one of the first developed markets central banks to cut policy interest rates. The BOC cut its rate target by 0.25 percentage points, to 4.75%. We expect another 0.25–0.50 points in rate cuts this year.

- We foresee continued progress in the inflation fight this year amid below-trend growth and still-restrictive monetary policy. A weaker labour market and a resulting easing of wage pressures should slow price increases for services unrelated to shelter. We foresee core inflation, which excludes volatile food and energy prices, ending 2024 in a range of 2.1%–2.4% on a year-over-year basis.

- We expect below-trend economic growth for the full year in a range of 1.25%–1.5% amid monetary policy restrictiveness that has been more potent than in the U.S.

- The unemployment rate (6.4% in June) is near the top of our year-end forecast range of 6%–6.5%, reflecting weak economic growth. Risks have increased that the unemployment rate could rise more than our forecast as still-restrictive monetary policy could eat into demand and, ultimately, corporate profitability.

Euro area

The euro area is growing again, with real GDP increasing by 0.3% in the first quarter compared with the fourth quarter of 2023, leaving behind five quarters of stagnation. We expect modest growth the rest of the year, supported by rising real incomes and lower inflation-adjusted borrowing costs. We foresee full-year GDP growth of 0.8%.

- Recent upside surprises in services inflation have led us to raise our year-end forecast for core inflation, from 2.2% to 2.6% year over year, and for headline inflation from 2.0% to 2.2%.

- The European Central Bank (ECB) left its deposit facility rate unchanged at 3.75% on 18 July. Its 0.25-percentage-points cut on 6 June ended a 4.5-percentage-point hiking cycle that began in July 2022. We expect the next rate cut to take place in September and quarter-point cuts quarterly thereafter, which would leave the policy rate at 3.25% at year-end 2024 and 2.25% at year-end 2025. However, risks skew toward less easing given a recent rise in services inflation.

- The unemployment rate held steady at a record low of 6.4% on a seasonally adjusted basis in May. We foresee the unemployment rate ending 2024 around current levels. However, lower corporate profit margins skew risks to the upside.

United Kingdom

Increased activity in the services sector drove a greater-than-expected gain in the last monthly GDP reading. GDP grew by 0.4% in May compared with April, the Office for National Statistics reported 11 July. Services output, the largest contributor to the monthly gain, increased by 0.3% month over month for a second straight month.

- Based on the stronger growth, Vanguard has raised its forecast for second-quarter and full-year GDP growth. We foresee growth of 0.7% in the second quarter compared with the first, leading us to increase our forecast for full-year growth from 0.7% to 1.2%. We anticipate only a marginal impact on growth from the new Labour government.

- We anticipate that the Bank of England (BOE) will start lowering interest rates—0.25 percentage points at a time, on a quarterly schedule—beginning in August, which would leave the bank rate at 4.75% to end 2024 and at 3.75% to end 2025.

- However, the recent increases in services and overall economic activity represent a risk to an August start of BOE rate-cutting and the number of cuts that might be made this year. Meanwhile, private-sector wage growth, excluding bonuses, has moderated but remains high, at 5.6% year over year in the March–May period. Finally, the BOE may be constrained if the Federal Reserve decides that it’s not in position to cut rates in 2024. Vanguard’s regional chief economists recently discussed the potential for central bank policy divergence.

China

As its leadership convened for a twice-a-decade economic policy meeting known as the 3rd Plenum, China released data 15 July showing the economy hit a soft patch. GDP grew by 0.7% in the second quarter compared with the first and by 4.7% year over year. Consumption lost momentum, reflecting weak domestic demand, sluggish imports, and subdued inflation.

- We continue to foresee economic growth of 5.1% for the full year, though supply and demand that remain out of balance could challenge that growth’s sustainability.

- We expect full-year core inflation to register about 1% and full-year headline inflation of 0.8%, which would be well below the 3% inflation target set by the People’s Bank of China (PBOC).

- Meanwhile, the PBOC has changed its monetary policy rate from the one-year medium-term lending facility (MLF) to the seven-day reverse repo rate. “When the PBOC created the MLF in 2014, it didn’t mean to create a new policy rate,” said Grant Feng, a Melbourne, Australia-based senior economist. “Its purpose was to manage money supply as an alternative to foreign exchange purchases and banks’ reserve requirement ratios.”

- The main shortcoming of the MLF, which became China’s key policy rate in 2019, is its weak relationship with short-term market rates. It has a much longer maturity than the policy rates of most other major central banks. In practice, Feng said, its weakness became evident in the last year. Because of weak credit demand, banks didn’t want to borrow from the MLF—currently at 2.5%—when they could get less expensive financing from other sources. The seven-day reverse repo rate currently stands at 1.8%. Vanguard foresees its being cut to 1.6% by year-end 2024.

Emerging markets

The central banks of Romania, the Czech Republic, and Hungary all cut rates in their last policy meetings as inflation in emerging Europe has moderated. In contrast, some Latin American central banks have—for now, at least—put rate cuts on hold.

- Banco Central do Brasil held its policy Selic rate at 10.5% on 19 June, having lowered it in the previous seven meetings. Policymakers said Brazil’s economic activity and labour market were stronger than expected and that an environment that included uncertainty about the Federal Reserve’s rate cycle “continues to require caution from emerging market countries.”

- Banco Central de Chile cut its policy interest rate, by 0.25 percentage points, to 5.75%, on 18 June. If its assumptions hold up, the bank said, the bulk of its 2024 rate reductions have already taken place. Cuts so far this year now total 2.5 percentage points.

- Banco de México (Banxico), which has cut rates once this year, on 27 June left its target for the overnight interbank rate unchanged at 11%. Vanguard anticipates an additional 0.75–1.25 percentage points of cuts in 2024, to a year-end range of 9.75%–10.25%.

Amid continued U.S. economic strength, we recently upgraded our forecast of GDP growth in Mexico. U.S. demand for Mexican goods has remained strong, and domestic wages and consumption are holding up. However, amid restrictive monetary policy, we foresee below-trend 2024 GDP growth of 1.75%–2.25%.

IMPORTANT: The projections and other information generated by the Vanguard Capital Markets Model® regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. VCMM results will vary with each use and over time.

The VCMM projections are based on a statistical analysis of historical data. Future returns may behave differently from the historical patterns captured in the VCMM. More important, the VCMM may be underestimating extreme negative scenarios unobserved in the historical period on which the model estimation is based.

The Vanguard Capital Markets Model is a proprietary financial simulation tool developed and maintained by Vanguard’s primary investment research and advice teams. The model forecasts distributions of future returns for a wide array of broad asset classes. Those asset classes include U.S. and international equity markets, several maturities of the U.S. Treasury and corporate fixed income markets, international fixed income markets, U.S. money markets, commodities, and certain alternative investment strategies. The theoretical and empirical foundation for the Vanguard Capital Markets Model is that the returns of various asset classes reflect the compensation investors require for bearing different types of systematic risk (beta). At the core of the model are estimates of the dynamic statistical relationship between risk factors and asset returns, obtained from statistical analysis based on available monthly financial and economic data from as early as 1960. Using a system of estimated equations, the model then applies a Monte Carlo simulation method to project the estimated interrelationships among risk factors and asset classes as well as uncertainty and randomness over time. The model generates a large set of simulated outcomes for each asset class over several time horizons. Forecasts are obtained by computing measures of central tendency in these simulations. Results produced by the tool will vary with each use and over time.

This article contains certain 'forward looking' statements. Forward looking statements, opinions and estimates provided in this article are based on assumptions and contingencies which are subject to change without notice, as are statements about market and industry trends, which are based on interpretations of current market conditions. Forward-looking statements including projections, indications or guidance on future earnings or financial position and estimates are provided as a general guide only and should not be relied upon as an indication or guarantee of future performance. There can be no assurance that actual outcomes will not differ materially from these statements. To the full extent permitted by law, Vanguard Investments Australia Ltd (ABN 72 072 881 086 AFSL 227263) and its directors, officers, employees, advisers, agents and intermediaries disclaim any obligation or undertaking to release any updates or revisions to the information to reflect any change in expectations or assumptions.

© 2024 Vanguard Investments Australia Ltd. All rights reserved.

July 2024

Vanguard

vanguard.com.au